Economics

Mar 26, 2026

Principles of Economics

Microeconomic Theory

Macroeconomic Theory

Econometrics

Statistics for Economics

International Economics

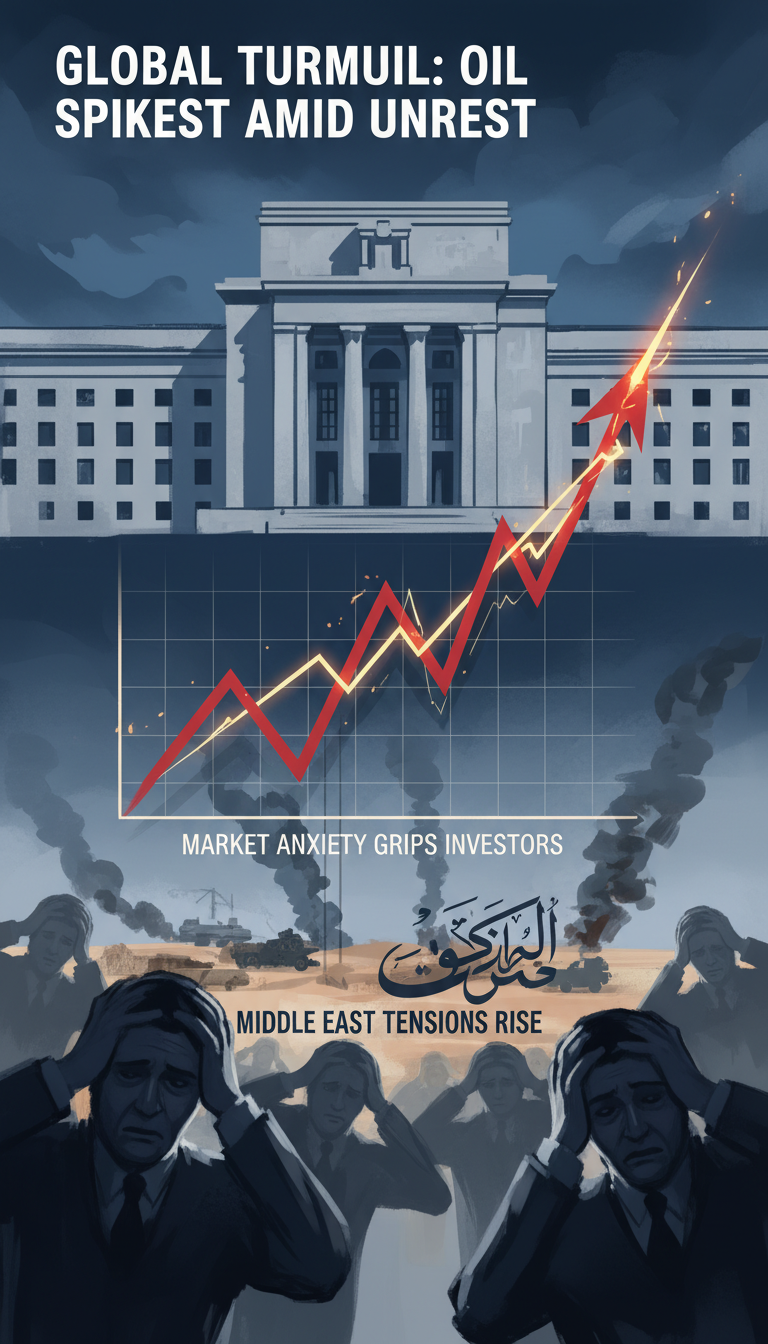

Why the Strait of Hormuz Shock Sent Oil Toward $120 — and Why It Didn’t Stay There

The 2026 Strait of Hormuz crisis jolted oil markets because a partial disruption at a tiny chokepoint can reprice energy worldwide. Here’s how selective passage, risk premiums, shi

The Strait of Hormuz crisis looks simple on the surface: war risk rises, oil jumps. But the deeper story is why partial disruption can move prices so violently — and why the market can also reverse before the physical flow is fully normalized. That missing layer is the difference between a scary headline and a real economic forecast.

Why a partial closure can still cause a major price spike

The Strait of Hormuz matters because it is not just another shipping lane. Roughly a fifth of global seaborne oil trade passes through it, along with major volumes of condensate and liquefied natural gas. When a chokepoint that important becomes uncertain, traders do not wait for a total shutdown to reprice oil.

That is because oil prices reflect expected future availability, not only barrels lost today. If markets think exports from Gulf producers could be delayed, rerouted, insured at far higher cost, or interrupted by military escalation, they add a risk premium immediately. Even if many tankers still move, the possibility of sudden disruption is enough to lift Brent sharply.

This is why the move toward $120 happened even though the strait was not completely sealed. A “porous” blockade still creates scarcity risk, timing risk, and panic hedging by refiners and importers.

Why prices fell back toward $100 instead of staying at crisis highs

The key reason is that the market learned the disruption was severe but selective. Iran reportedly allowed passage for “non-hostile” shipping rather than enforcing a full stop on all traffic. That changed the pricing logic from catastrophic supply loss to managed disruption with escalation risk.

In practical terms, that means traders began removing part of the extreme war premium. Prices can fall even while conditions remain dangerous if the worst-case scenario becomes less likely. That appears to be what happened as Brent retreated from around $120 to near $100.

So the answer to one big question is clear: oil did not stay at $120+ because the market stopped pricing a full, sustained closure as the base case. It shifted to a middle scenario — costly disruption, but not total paralysis.

Explore our free economics courses

Principles of Economics

University · Economics

Microeconomic Theory

University · Economics

Macroeconomic Theory

University · Economics

Econometrics

University · Economics

Statistics for Economics

University · Economics

International Economics

University · Economics

How the shock reaches inflation, gas prices, and recession risk

Oil is a global benchmark market, which is why U.S. consumers are not insulated just because America produces a lot of shale oil. Domestic fuel prices still respond to world crude prices, refinery constraints, and diesel demand.

Higher crude feeds through the economy in layers:

- Gasoline and diesel become more expensive, raising household and freight costs.

- Shipping and insurance costs rise as tankers face danger premiums and rerouting delays.

- Petrochemicals and fertilizers get more expensive, pushing up costs for plastics, packaging, and food production.

- Central banks face a harder tradeoff if inflation rises while growth slows.

That last point is why markets worry about recession. An oil shock acts like a tax on consumers and businesses. If it lasts long enough, spending weakens, margins shrink, and growth forecasts fall.

What determines whether this becomes a short shock or a deeper economic hit

Two variables matter most.

1. Duration of disruption

A brief crisis mainly adds volatility and precautionary buying. A disruption lasting weeks can drain inventories, raise fuel prices more broadly, and start affecting industrial output and consumer confidence.

2. Whether military action restores confidence or widens the war

Military operations do not automatically calm markets. If they secure shipping lanes without broadening the conflict, prices may ease further. But if they trigger attacks on more tankers, ports, or regional energy infrastructure, the premium can surge again very quickly.

So to answer the second big question: what decides whether prices spike again or keep easing is not just whether ships can pass, but whether markets believe that passage is durable, insurable, and politically stable.

The overlooked winners, losers, and workarounds

Not every player is hurt equally. Energy exporters outside the immediate conflict zone can benefit from higher prices. Russia gains from stronger crude and tighter petrochemical and fertilizer markets. China may gain bargaining leverage and trade opportunities if it can secure flows others struggle to access.

Meanwhile, import-dependent economies in Europe and Asia face the biggest inflation exposure. Alternative routes and ports, including Saudi infrastructure linked to Red Sea export options such as Jeddah, become more valuable — but they do not fully replace Hormuz capacity.

This is the broader lesson: chokepoint crises do not need to stop all trade to reshape pricing power, trade flows, and geopolitical leverage.

Bottom line

The Strait of Hormuz shock pushed oil toward $120 because markets priced the risk of losing access to one of the world’s most important energy arteries. Prices then fell back because the disruption proved partial, not absolute, and traders reduced the odds of a sustained worst-case closure.

If the current selective passage holds, the damage may remain painful but manageable. If confidence in that passage breaks, the next move in oil will depend less on headlines about “open” or “closed” and more on whether the world believes the flow is truly secure.