Economics

Mar 23, 2026

Principles of Economics

Microeconomic Theory

Macroeconomic Theory

Econometrics

Statistics for Economics

International Economics

Why the Fed Froze Rate Cuts as Oil Spiked — and What Would Change Its Mind

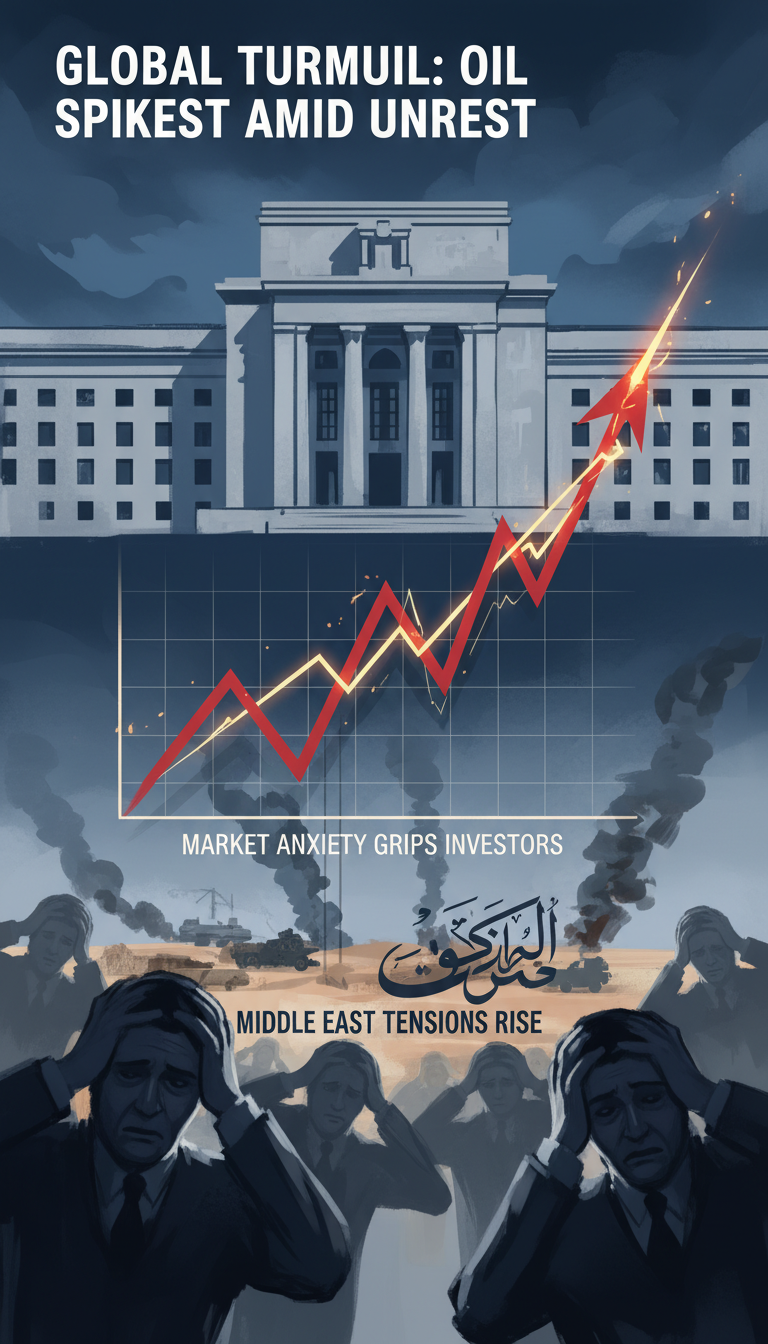

The Fed held rates steady and cut its 2026 easing outlook after the Iran war sent oil sharply higher. Here’s how an oil shock can move from gas pumps into inflation policy, why off

The headline looked simple: the Federal Reserve held rates steady and signaled fewer cuts. But the deeper story is not just “oil up, cuts down.” The real issue is whether a war-driven energy shock stays temporary or seeps into the rest of the economy. That is the layer markets, households, and the Fed are all trying to read at once.

What changed the Fed’s outlook so quickly?

Before the Iran war, investors expected a gentler inflation path and more room for rate cuts. Then oil surged, with Brent jumping from roughly $70 to above $107 and briefly touching even higher levels. That matters because energy is one of the fastest ways a geopolitical shock hits consumer prices.

The Fed now expects inflation to end the year higher than previously forecast, even while still seeing decent growth and some labor-market cooling. That combination creates a policy trap: if officials cut too early, they risk validating a new inflation wave; if they stay tight too long, they risk worsening unemployment and slowing the economy more than necessary.

That is why Chair Powell emphasized uncertainty and why reports said even a rate hike was discussed. The message was not that hikes are likely, but that the range of outcomes has widened sharply.

Explore our free economics courses

Principles of Economics

University · Economics

Microeconomic Theory

University · Economics

Macroeconomic Theory

University · Economics

Econometrics

University · Economics

Statistics for Economics

University · Economics

International Economics

University · Economics

How does an oil shock actually reach Fed policy?

Oil does not just raise gasoline prices. It can spread through the economy in stages.

- Direct effect: households pay more for gas, heating, air travel, and shipping-linked goods.

- Business cost effect: firms facing higher transport, plastics, chemicals, and logistics costs may raise prices.

- Expectation effect: if workers and businesses start assuming inflation will stay high, wage demands and price-setting behavior can shift.

- Core spillover: what began as an energy shock can broaden into services and other “core” categories the Fed watches closely.

The Fed can often “look through” a short-lived oil spike if it believes the shock will fade. But it becomes much harder to ignore if inflation expectations drift up or if supply disruptions last long enough to affect wages, freight, and everyday pricing decisions.

Will this oil shock fade — or spread into core inflation?

That is the central question. Not every oil spike becomes a lasting inflation problem. Sometimes prices jump, consumers absorb the hit, and inflation cools once energy markets stabilize. But wars create a different risk because they can disrupt shipping, insurance, business confidence, and supply chains all at once.

The biggest edge case is the Strait of Hormuz. If the conflict threatens that route, markets will not just price current supply losses; they will price the risk of a much larger disruption. That can keep oil elevated long enough for “temporary” inflation to become more persistent.

Today is not the 1970s: the US economy is less oil-intensive, the Fed is more credible, and wage indexation is weaker. Still, the lesson from history is that central banks get into trouble when they assume an energy shock will stay neatly contained and it does not.

Why are Fed officials so divided?

The dot plot split makes sense once you see the trade-off. Hawks focus on inflation persistence: if oil feeds into broader prices, cutting too soon could force the Fed to reverse course later. Doves focus on the labor market: if hiring weakens and real incomes are squeezed by energy costs, high rates could become unnecessarily restrictive.

That is why some officials still see a cut, some see none, and a smaller group sees more easing. They are not merely disagreeing about ideology. They are making different bets about transmission: does this remain an energy shock, or does it become a broader inflation regime?

What would make the Fed cut later this year — or wait even longer?

A cut becomes more likely if two things happen together: oil prices stabilize or retreat, and core inflation measures stop showing spillover from energy into broader categories. The Fed would also want clearer evidence that labor-market softening is becoming more serious than inflation risk.

On the other hand, the Fed is likely to stay on hold longer if:

- oil remains elevated for months rather than weeks,

- inflation expectations rise,

- core services inflation stays sticky, or

- the war threatens major shipping routes and global supply chains.

In other words, the next move is not mainly about one oil price print. It is about whether the shock broadens and whether the economy absorbs it without a second inflation wave.

The bottom line

The Fed did not simply panic over headlines from the Middle East. It paused because oil shocks matter less for their first move than for their second-round effects. If the war-driven spike fades, cuts can come back into view. If it spreads into core inflation and expectations, the Fed may stay tight far longer than markets once assumed.

So the two questions that matter most are now clear: will the oil shock stay temporary or leak into core inflation, and what exact evidence would convince the Fed to cut anyway? For now, that is the real policy battlefield.