Economics

Mar 22, 2026

Principles of Economics

Microeconomic Theory

Macroeconomic Theory

Econometrics

Statistics for Economics

International Economics

Why the Fed Held Rates Steady Even as War Threatens New Inflation

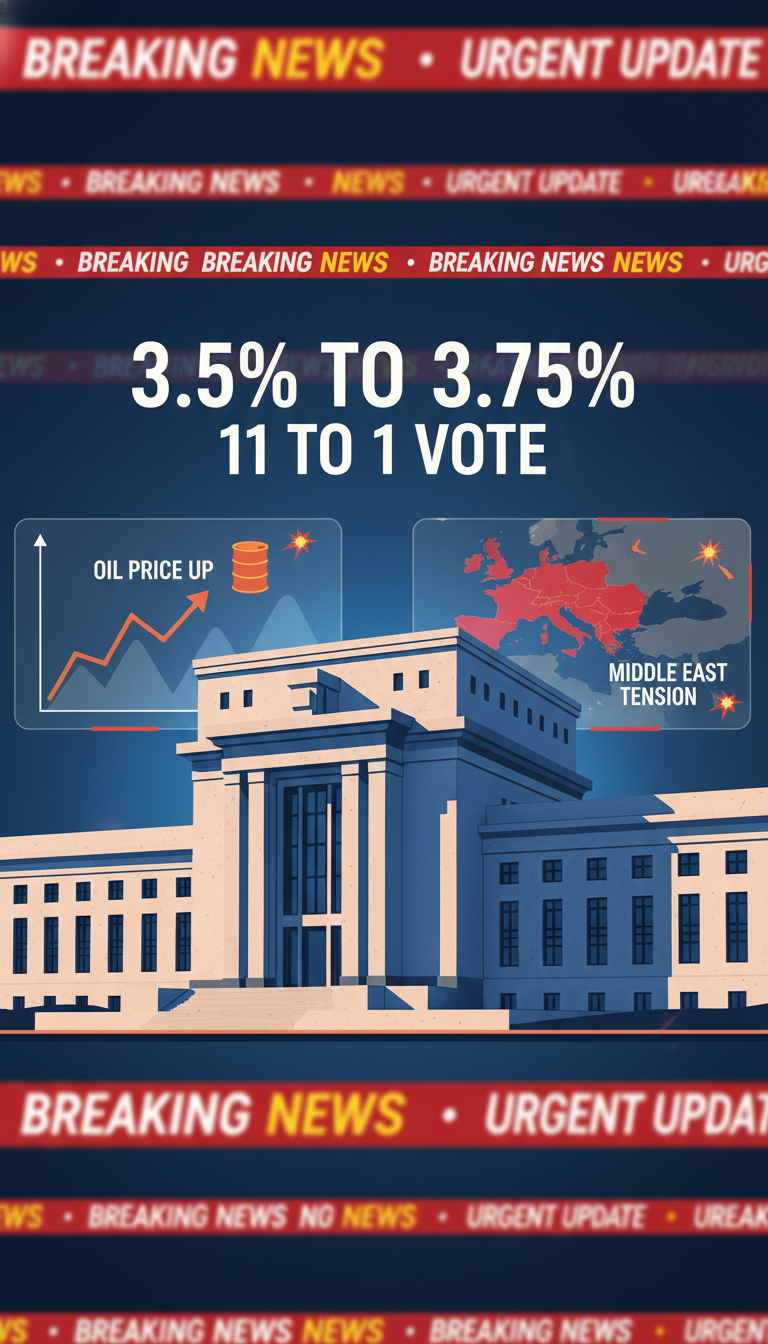

The Federal Reserve kept rates at 3.5%–3.75% despite rising oil-driven inflation risks tied to the US-Israel war with Iran. Here’s the real logic behind that decision, what could c

The surprising part of the Fed’s March 2026 decision was not just that it held rates steady. It was that officials did so while openly acknowledging that war-related energy shocks could push inflation higher, and still kept one quarter-point cut in their 2026 outlook. That looks contradictory on the surface. It makes more sense once you separate the inflation the Fed can influence from the inflation it mostly has to absorb and monitor.

Why the Fed did not rush to hike

The federal funds rate works mainly by cooling demand: borrowing, spending, hiring, and investment. But an oil shock from war is first a supply shock. If conflict disrupts production or shipping, gasoline, diesel, jet fuel, and petrochemical inputs get more expensive regardless of whether the Fed moves rates by 25 basis points.

That is why central banks usually do not react mechanically to the first jump in oil prices. A rate hike cannot pump more crude, reopen shipping lanes, or lower insurance costs in a conflict zone. If the Fed tightened immediately, it could weaken growth without fixing the original cause of the price spike.

So holding steady was not complacency. It was a signal that officials want to see whether the shock stays narrow and temporary, or spreads into broader inflation.

What would make the Fed scrap its projected cut?

The key threshold is not simply “oil is up.” It is whether higher energy prices create second-round effects across the economy. The Fed can tolerate a temporary rise in headline inflation more easily than a broad reacceleration in underlying prices.

Officials would be more likely to drop their planned 2026 cut if several things happen at once:

- Gasoline and energy prices stay elevated for months rather than weeks.

- Core inflation measures begin rising, not just headline CPI.

- Businesses pass fuel and transport costs into a wider range of goods and services.

- Workers begin demanding higher wages to offset living-cost increases.

- Inflation expectations move up in surveys or market pricing.

That is the real policy danger: not the initial oil spike, but the moment it starts changing pricing behavior and wage-setting throughout the economy.

Explore our free economics courses

Principles of Economics

University · Economics

Microeconomic Theory

University · Economics

Macroeconomic Theory

University · Economics

Econometrics

University · Economics

Statistics for Economics

University · Economics

International Economics

University · Economics

How war inflation reaches CPI and the Fed’s target

The transmission usually follows a chain. First comes crude oil. Then refining and distribution costs lift gasoline, diesel, and aviation fuel. After that, freight, delivery, air travel, food production, plastics, chemicals, and other energy-intensive sectors feel the pressure. Some firms absorb the hit; others raise prices.

This is why headline CPI can move quickly, while broader measures such as core inflation or PCE may react more slowly. The Fed targets 2% inflation over time and pays close attention to whether a shock remains concentrated or becomes generalized.

History matters here. The 1970s taught central bankers that repeated energy shocks become much more dangerous when they feed expectations and wages. But history also taught them not to overreact to every commodity spike as if it were automatically a 1970s replay.

Why one rate cut is still in the forecast

The Fed’s projection of one cut later in 2026 reflects a balancing act, not optimism. CPI was still around 2.4% entering the meeting, the labor market remained reasonably balanced, and growth had not collapsed. In other words, the economy had not yet produced the kind of broad inflation breakout that would force a more hawkish path.

Keeping one cut in the outlook also preserves flexibility. If the oil shock fades, shipping stabilizes, and core inflation stays contained, the Fed could still ease modestly without losing credibility. The single dissenting vote shows that not everyone is comfortable with that judgment, but the majority appears to believe the evidence is not yet strong enough to preemptively tighten.

The June and July data that now matter most

If you want to know whether that projected cut survives, watch a short list of indicators:

- Headline CPI and PCE: Are energy effects accelerating?

- Core CPI and core PCE: Is inflation spreading beyond fuel?

- Average hourly earnings and employment data: Are wages responding to higher living costs?

- Inflation expectations: Do households and markets think higher inflation will last?

- Oil and shipping conditions: Is the war shock easing or becoming persistent?

If June and July show only a temporary energy bump, one cut remains plausible. If they show broadening price pressure, the Fed may have to abandon that plan.

Bottom line

The Fed held steady because monetary policy is a blunt tool against a war-driven oil shock. What matters now is whether the shock stays mostly in energy or leaks into core inflation, wages, and expectations. That is also the answer to the two big questions hanging over this decision: the projected cut disappears if inflation broadens and persists, and the June/July data that matter most are the ones that reveal whether this is still an oil story or the start of a wider inflation problem.