Economics

Mar 22, 2026

Principles of Economics

Microeconomic Theory

Macroeconomic Theory

Econometrics

Statistics for Economics

International Economics

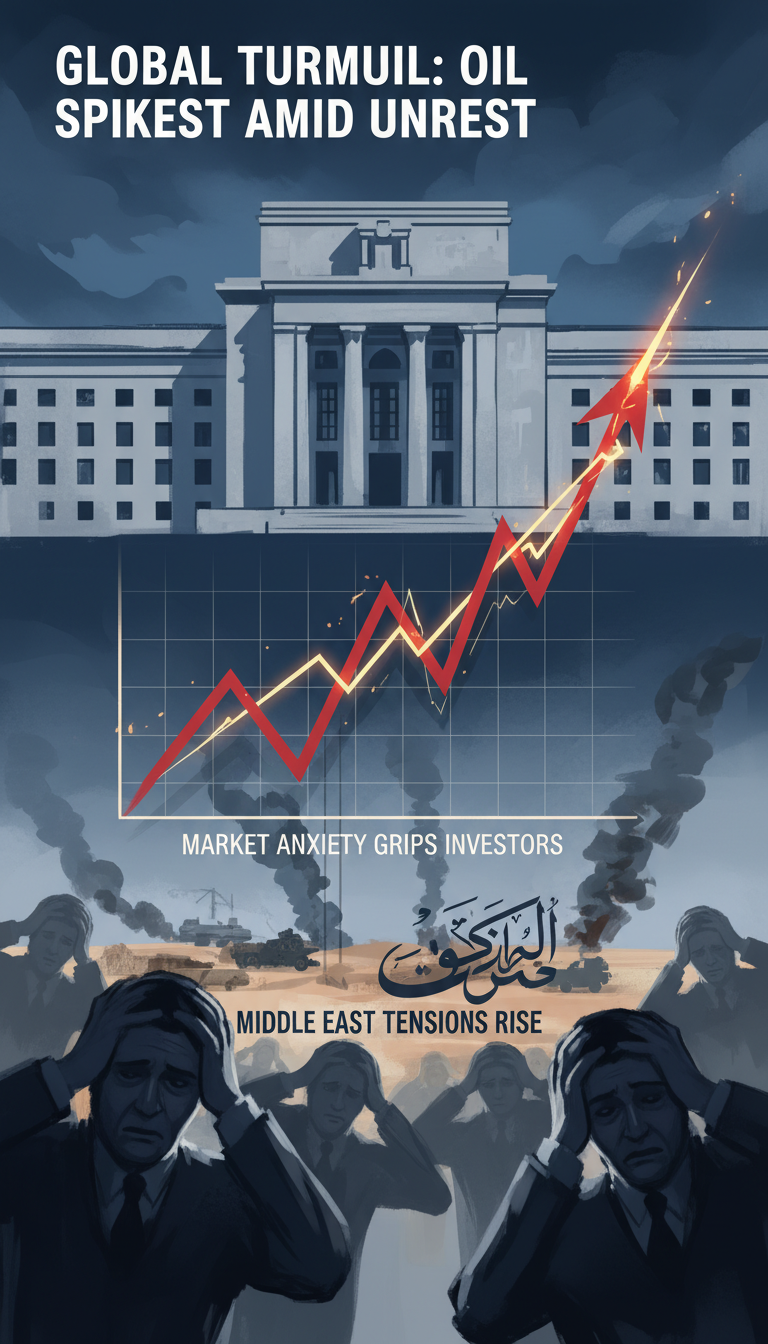

Why Oil Above $100 Matters More Than the Headline: The Real Economic Damage From a Hormuz Shock

Oil has surged past $100 a barrel after war-related disruptions in the Middle East. Here’s what actually drives the spike, why the world economy still gets hit even if the US pumps

Oil crossing $100 a barrel is not just a scary market headline. In this case, the deeper issue is why prices jumped so fast: not a routine production cut, but a war-driven disruption to one of the world’s most important energy chokepoints. That changes how long the shock can last, how much damage it can do, and why even countries that produce a lot of oil are not automatically protected.

Why this spike is different from ordinary oil volatility

Oil prices often jump on fear, then fall when traders calm down. This time, the market is reacting to a physical supply problem. If the Strait of Hormuz is effectively disrupted and Gulf exports are delayed or halted, the world is not merely pricing risk; it is pricing missing barrels.

That distinction matters because the reported shortfall is enormous. A disruption on the order of 8 to 10 million barrels per day is close to 10% of global oil supply. At that scale, inventories, emergency reserves, and rerouted shipping can soften the blow, but they do not fully replace the lost flow. That is why prices can stay elevated even after governments announce reserve releases.

How a shipping disruption becomes a global economic shock

The mechanism is straightforward but brutal. Oil is globally traded, so the key issue is not just production at the wellhead; it is whether crude can be loaded, insured, shipped, refined, and delivered on time. If tankers cannot move safely through Hormuz, then even output that still exists becomes harder to use.

Explore our free economics courses

Principles of Economics

University · Economics

Microeconomic Theory

University · Economics

Macroeconomic Theory

University · Economics

Econometrics

University · Economics

Statistics for Economics

University · Economics

International Economics

University · Economics

That creates several layers of pressure at once:

- Physical scarcity: refiners compete for fewer accessible barrels.

- Shipping and insurance costs: war risk raises the delivered price further.

- Panic buying: countries and firms build precautionary inventories.

- Knock-on fuel costs: gasoline, diesel, jet fuel, and petrochemicals all rise.

From there, the shock spreads beyond energy. Airlines, trucking, manufacturing, farming, and consumer goods all face higher costs. Households then spend more on fuel and less on everything else, which is how an oil shock starts dragging on growth.

Why the US is not insulated, even as a major producer

A common misconception is that the United States can shrug off high oil prices because it is a major producer and a net exporter in some categories. Higher prices do help some domestic producers, especially shale companies, and can boost profits, drilling incentives, and energy-sector investment.

But that does not cancel the broader hit. American consumers still buy gasoline priced off global crude markets. US businesses still pay more for transport and inputs. And shale cannot instantly replace a multi-million-barrel-per-day disruption; drilling, completion, labor, pipelines, and export logistics all take time.

So the answer to one key question is clear: the world economy still gets hit because oil is globally priced and globally transported, and a chokepoint disruption raises costs far beyond the countries directly involved in the war.

What determines whether prices stabilize or keep climbing

The second big question is what would actually bring prices down. The short answer is that stabilization depends less on trader psychology than on logistics and duration.

Prices are more likely to stabilize if several things happen together:

- Tanker traffic resumes through Hormuz with credible military protection and lower insurance risk.

- Export infrastructure remains intact so producers can actually load cargoes.

- Strategic reserves are released at scale to bridge the immediate gap.

- Non-Middle East supply rises from shale, Brazil, Canada, or others.

- Demand weakens enough to reduce competition for barrels.

If those conditions do not materialize, prices can remain high or rise further because the market keeps repricing a prolonged shortage. In other words, oil stabilizes when transport reliability returns and replacement supply becomes believable, not simply because prices look “too high.”

The inflation and recession risk is real

At $100-plus oil, central banks face a familiar problem: inflation pressure rises even as growth slows. That is the uncomfortable mix that makes energy shocks so dangerous. If the spike lasts only briefly, the damage may be manageable. If it lasts for months, the hit to global GDP can become large enough to materially raise recession risk.

This is why comparisons to the 1970s keep appearing, though today’s economy is not identical. The major difference is US shale, which gives the world more flexibility than it had decades ago. The limit is speed: shale is a cushion, not a magic switch.

Bottom line

Oil above $100 matters because this is not just a speculative spike; it is a war-driven supply and shipping shock centered on a critical global chokepoint. The world economy gets hurt even if some producers benefit, because fuel prices, transport costs, and inflation spread through everything. And prices will only truly stabilize when the physical flow of oil becomes reliable again, especially through Hormuz, or when enough replacement supply and demand adjustment close the gap.