Economics

Mar 26, 2026

Principles of Economics

Microeconomic Theory

Macroeconomic Theory

Econometrics

Statistics for Economics

International Economics

Why Markets Erased 2026 Fed Rate Cuts Even After the Fed Still Projected One

Markets now price essentially zero chance of any 2026 Fed rate cuts, despite the Fed’s own dot plot still showing one. Here’s what that divergence really means, what mechanism drov

The striking part of the latest Fed story is not just that rates were held steady. It is that, almost immediately after the March 2026 meeting, markets moved to price zero chance of any rate cuts this year, even though the Fed’s own dot plot still pointed to one 25-basis-point cut. That gap matters because it reveals a deeper fight over how inflation works, how much oil shocks can spill into the broader economy, and whether the Fed is closer to done tightening than investors think.

What “zero chance of cuts” actually means

A common misconception is that tools like CME FedWatch, fed funds futures, and overnight index swaps are official forecasts. They are not. They are market prices that imply where traders think the policy rate will land, based on incoming data, risk premiums, and hedging demand.

So when swaps imply a 0% chance of 2026 cuts, that does not mean the Fed announced no cuts. It means traders collectively decided that, given current information, the most likely path is rates staying where they are or even moving slightly higher.

That distinction explains the apparent contradiction: the Fed can still project one cut while markets refuse to believe it.

Why traders turned so quickly after the FOMC

The mechanism is straightforward but powerful. Markets reprice when the expected path of inflation and growth changes. After the meeting, several forces pushed in the same direction:

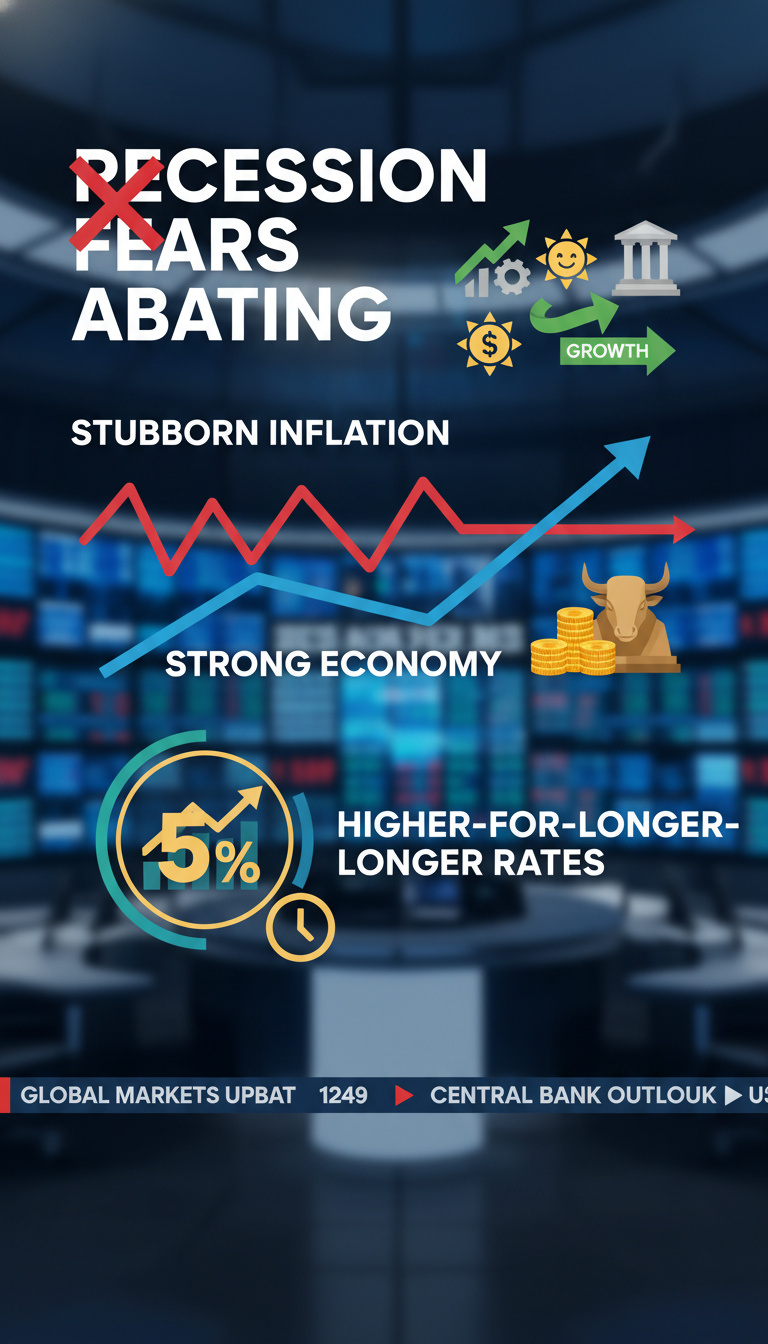

- Sticky inflation: core PCE forecasts moved up, suggesting price pressures are not cooling fast enough.

- Resilient growth: the economy has slowed less than many expected, reducing the need for rate relief.

- Labor market durability: even with flat or weak net job growth in some readings, unemployment and broader activity have not collapsed.

- Oil shock risk: rising energy prices tied to Middle East conflict raise the chance of headline inflation reaccelerating.

- Powell’s tone: his comments signaled confidence in the economy’s ability to absorb shocks, not urgency to cut.

Put together, that shifts the distribution of outcomes. Instead of “one cut unless something goes wrong,” traders moved toward “no cuts unless inflation clearly breaks lower.”

Explore our free economics courses

Principles of Economics

University · Economics

Microeconomic Theory

University · Economics

Macroeconomic Theory

University · Economics

Econometrics

University · Economics

Statistics for Economics

University · Economics

International Economics

University · Economics

Why oil matters more than the headline suggests

One barrel of expensive oil does not automatically force a Fed hike. The deeper issue is whether an oil spike stays isolated or spreads through transport costs, goods prices, inflation expectations, and wage demands.

That is why the market reaction has been so sharp. If geopolitical conflict keeps energy elevated for months, the Fed faces a familiar problem: growth may still look decent while inflation stops improving. That is the essence of a stagflation scare.

Powell has pushed back on the idea that the US is already in stagflation. But markets are not waiting for that label. They are pricing the possibility that inflation becomes sticky enough to block cuts, even if growth remains positive.

Why the dot plot and the market can disagree for so long

The dot plot is not a promise. It is a snapshot of individual policymakers’ expectations under their current assumptions. Markets, by contrast, update continuously and often assign more weight to tail risks.

That means divergence can persist when traders think the Fed is underestimating one of three things:

- the persistence of inflation,

- the inflationary effect of oil, tariffs, or fiscal policy, or

- the economy’s ability to tolerate high rates without cracking.

In other words, markets are not necessarily saying the Fed is wrong today. They are saying the Fed may have to revise its own outlook later.

What would make cuts return — or hikes become real

Two concrete developments would bring markets back toward the Fed’s one-cut view. First, inflation data would need to show renewed progress, especially in core services and shelter-related measures. Second, labor-market softness would need to broaden beyond isolated weak prints into a clearer slowdown in hiring, hours, or wage growth.

On the other side, hikes become more plausible if oil stays high long enough to lift inflation expectations, or if tariffs and fiscal policy add fresh price pressure while growth remains firm. That is why some contracts now show a nontrivial chance of rates ending 2026 higher, not lower.

What this means for investors and the broader economy

A no-cut world is not automatically a recession signal. In this case, it can mean the opposite: the economy is strong enough, and inflation sticky enough, that the Fed does not need to ease. That tends to support cash yields and short-duration bonds, while pressuring rate-sensitive assets that were counting on cheaper money.

The bigger implication is psychological. For months, many investors were trained to expect cuts as the default next move. Markets are now challenging that assumption. The question is no longer “when will easing begin?” but “what evidence would be strong enough to justify it?”

The market erased 2026 cuts because traders now see inflation risks, oil shocks, and economic resilience outweighing the case for relief. And the Fed-market split persists because the dot plot reflects current official assumptions, while futures price the possibility those assumptions will fail. The next CPI and jobs reports will matter, but so will whether energy and policy shocks fade or spread through the economy.